Indexed universal life insurance (IUL) is an innovative, low risk type of permanent life insurance. It is primarily intended for people interested in long term life insurance coverage and tax favorable distributions, typically during retirement. These policies are well suited for life insurance buyers seeking large policies, known as jumbo life insurance policies. For premium financing, some consumers prefer to use an indexed product (see reasons below). The use of indexing strategies guarantees there will a loss of cash value when markets are down. No market losses makes IUL an appealing product for risk averse consumers. The fact that 0% is the lowest crediting rate possible makes it worthy of consideration, especially when the stock market is down 30%. The interest credited to IUL policies will never be below 0%. In fact, some products guarantee a floor of one or two percent.

Do IUL policies reduce risk for life insurance buyers? Since none of the policy’s cash value is ever invested directly in the stock market, it does provide a buffer against normal market volatility. “Zero is your hero” feels pretty good when markets are down 25%. Market losses during these market cycles can be quite damaging.

We might think that dynamite and an IUL insurance policy are nothing alike. One is an explosive and the other is often described as another boring type of life insurance policy. While that may be true, in the wrong hands, dynamite can be catastrophic. In a professional’s hands, dynamite can be part of a well controlled plan to bring down a multi-story building without much of a fuss. In the wrong hands, an IUL policy can make a big mess and create nothing but unintended future problems. Properly used by a professional, an IUL policy can be the ideal product choice. Not all buildings should be brought down with dynamite and not all insurance plans call for IUL.

The use of indexing strategies may result in buying a policy with the lowest possible net cost of any policy measured in the medium and long term. Of course, this depends on how markets perform, the sequence of returns, how the policies are credited and how often and when the insurance companies lower the cap or participation rates. In order to achieve optimal returns, a greater level of understanding and responsibility by the policyowner is essential. It is definitely not a set it and forget it type of life insurance policy, unlike whole life. With the proper amount of education, indexed universal life is suitable for the following insurance buyers:

- Between ages 25-55 (ideally).

- Want permanent life insurance.

- Appreciate flexibility.

- Consistent, high income.

- High net worth.

- Interested in retirement income.

- Considering premium financing.

- Willing to routinely review inforce policies.

Like other permanent life insurance contracts, IUL builds up tax deferred cash value when interest is credited to the policies. A number of well-known indexes, such as the S&P 500 or the Nasdaq-100 are typical indexes options. There are no government imposed restrictions or limitations on contributions or distributions, like there are with qualified retirement plans. The cash value can be accessed without penalties or taxes, unlike a 401(k) or IRA. These policies are often used as private pension plans by people without access to a corporate pension plan.

There are policy expense charges and fees in IUL policies that should be understood by the agent and the policyowner. In good contracts, the fees are capped, which means they are less impactful as the premium levels increase. Indexed Universal Life is not a good alternative to term insurance or other products that do not build up cash value. It is most beneficial for younger consumers who want permanent insurance, flexibility, strong potential upside and tax free withdrawals near retirement.

The advantage of a policy that guarantees to never lose principal due to market performance can be compelling. Another reason for IUL’s popularity is because it is a powerful tool that smooths out returns. “The key to minimizing sequence of return risk is to reduce volatility, which IUL does far more than the S&P 500”, says Sam Rocke, SVP at Ash Brokerage.

Insurance companies share in the index’s upside when markets are up. They do this with simple cap rates and/or participation rates. For example, if the S&P is up 20% one year, a policy with a cap rate of 12% will credit the policy with 12% interest that year. Essentially, cap rates and participation rates create a partnership between policyholders and the insurance company. The insurance companies take all the risk.

The results are impressive as consumers are flocking to the safety of indexed universal life insurance. The product had $2.3 billion in sales for 2019 and the first half of 2020 saw more of the same record breaking growth.

Why Universal Life Insurance?

The retirement vehicle for many corporate employees is a 401(k). There is market risk with 401(k)s which is fairly well understood by individual investors. In addition to the market risks they assume, there are contribution limits, taxes that are deferred until withdrawal time as well as substantial recurring fees. For many, a 401(k) may not be the perfect retirement solution, by itself. Near retirement, the loss of principal is too costly. For others, they want the option to make flexible and much larger contributions than 401(k)s or IRAs allow. For these people, an indexed universal life policy can be an excellent addition to the other investment vehicles.

The stock market is volatile and it has been known to punish short term and medium term investors. Once people can see retirement in their future, a growing number of them begin to feel differently about the inherent risks in the stock market. Principal protection quickly becomes their main concern, rather than maximum yield. Yield is undoubtedly important, but an extra 1% is not worth exposing principal to drops of 30%.

What are the costs? Funded properly, these policies should have sufficient internal growth to offset the increasing cost of insurance charges and other internal fees. The current cost of insurance expenses and fees are subject to change and they are deducted from the cash account each year. Managed and funded properly, the account values should outpace annual deductions. I have many younger IUL clients who began funding their IUL contracts with oversized premium contributions. They benefit in two ways by doing that. Overfunding creates a cushion of cash value that can be used if income takes an unexpected hit and overfunding in good years can help in smoothing out the returns.

What is Universal Life? Some history about this product is beneficial. In the 1970’s, the rate of return of whole life insurance was 2-3%. When interest rates shot up to historic rates in the late 70’s and the 1980’s, EF Hutton created a flexible, interest sensitive product to compete against whole life. Other life insurance companies followed, with some crediting more than 12% at the time. Sales of universal life were meteoric. Billions of premiums poured into these contracts. As a young agent during this time, there was insufficient agent education about the impact of interest rates on long term policy performance. Policies sold based on double digit projections were destined for trouble.

As interest rates gradually decreased, new projections should have been provided to policyholders, by their agents. If a policy was purchased using illustrations based on 10% assumptions, it should have been re-projected again when rates fell to 6% and again when rates fell to 4% and again when they fell to the guaranteed rates in the contract. LOWER INTEREST RATES WILL CAUSE THE POLICY TO NEED MORE PREMIUM TO MEET THE PROJECTIONS THAT WERE BASED ON HIGHER RATES. WHEN THESE POLICIES WERE NOT FUNDED WITH THE HIGHER PREMIUMS NEEDED TO OFFSET THE LOWER CREDITING RATES, THE POLICIES TURNED INTO TICKING TIME BOMBS.

Adding insult to injury, when the looming crisis in a policy isn’t detected, it may leave the policyholder with no options. It’s like driving towards the edge of a cliff in the dark. You have no idea until it’s too late. The problem happens faster for older policyholders. For most agents, companies and policyholders, these were tough lessons. They taught us the value of regular reviews and to project life insurance conservatively. Things change that affect policies. The problem is not universal life. The problems were aggressive insurance company projections, insufficient agent education.

Indexed universal life (IUL) is not a “set it and forget it” type of policy to own. There are other policy types that are much easier to manage. Every potential IUL buyer should only work with an experienced life insurance professional familiar with indexing strategies. Choosing the right life insurance company is more critical than ever with this type of policy. Some companies are new to IUL and others have been real innovators and pioneers over the past 20 years. These are things the right life insurance professional will share with you.

Indexing Strategy Offers Best Of Both Worlds.

Most people may know that the stock market index has returned approximately 8% over the long term but less than 4% for average investors over the same time frame.

A variety of reasons are attributable for this gap. The biggest factor is emotion. Investors make all types of investment mistakes for many different reasons. Some are due to panic and some are due to their understandable inability to devote enough time and attention. Not only do investors have to be willing to commit the time, they also have to be ready to act every time action is required. Too many find that impossible while they are working, running businesses and caring for families.

Individual investors can never take their eye off the ball. Failing to buy and sell at the perfect times make it impossible to attain the average long term historical rates of return.

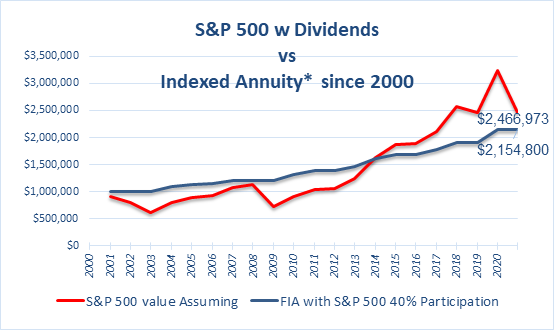

Timing the market is tough, even for professionals. When mistakes occur, they impact the overall yield. Warren Buffett says the first rule of investing is to never lose money and he’s right. But to do that, you must be laser focused at all times. Using an IUL prevents investors from ever losing money due to stock market returns.

IULs have a minimum rate of return, usually between 0% and 2%. For example, if you have $200,000 in a stock account and it drops 20%, you will be down by $40,000. The account value starting in the next year would be $160,000 (minus any fees). In the IUL policy, the same 20% market loss would result in the cash value remaining at $200,000 (minus any fees).

The Concept of Stacked Gains. The importance of stacked gains can not be stressed enough when markets are up. A 10% gain in the following year would result in new interest being credited to the policy in the amount of $20,000, putting the policy’s value at $220,000 at the end of the second year. In the stock account, there would be $160,000 plus the same 10% for year two growth (minus fees). The stock account value at the end of the second year would be $176,000 (minus fees).

The comparison is $220,000 in the IUL versus $176,000 in the stock account. From that point forward, the new base in the IUL is $220,000, never to go lower than that from market losses. Over time, protecting your principal from market loss, makes a huge difference in the policy’s accumulated savings. The cash value in an IUL can drop due to cost of insurance charges and/or fees. It shouldn’t happen but it is something to discuss with a life insurance professional at the point of purchase.

The Upside (cap rates) and the Downside Protection (the floor).

If never losing any principal due to negative market returns still sounds too good to be true, let’s peel back the onion a little bit. Quite simply, they are buying options to insure the downside guarantee that your policy will never lose principal from market losses. Life insurance companies employ some of the sharpest minds in the investment world to manage these assets. The people they have working for them are dedicated to nothing else. There can be billions of dollars allocated in these strategies.

Life Insurance Premium Financing

Using IUL contracts for premium financing is another strategy we use when it is appropriate for individuals to finance a policy. Today, it is the lure of low interest rates that makes financing a consideration. Premium financing should only be for high net worth individuals with at least $5,000,000+ of net worth. A person who needs permanent life insurance but does not want to use their own capital to pay the premiums is a good candidate for premium financing. An arbitrage should exist between the cost of the premium finance loan and the policyowner’s return on investment. For example, HNW people with an ROI of 10% on their assets can borrow the premiums today at 2% and for them, that may be ideal. That creates an 8% arbitrage and some lenders will gladly lock in longer term rates with favorable terms.

The goal of a premium financing strategy is to pay off the loan and be left with a properly funded life insurance policy, payable at death. With more than 30 years of premium finance experience and having placed over 600 financed policies, I have strong relationships with traditional lenders and specialty lenders that work with our clients to finance these policies. Many of our clients have their own banking relationships and they prefer doing business with them. In those cases, our job is to guide them through the insurance company requirements. You can learn more about premium financing here.

Policy Design

The way in which an IUL is initially designed is determined by the goals and objectives of the policyholder. For example, when using the policy to maximize tax-free income in retirement, the policy should be maximum funded, meaning the initial death benefit is low. A lower death benefit will result in less cost of insurance charges.

Is there a “best index or design” to choose? There is no way to know which indexed strategy will perform the best, either over the long term or the short term. We encourage our clients to work with professionals who will follow “best practices” when recommending index strategy allocations. That includes proper understanding of the index choices in order to make the right decision about which fund or funds to select.

Taxation – Indexed Universal Life Receives Favorable Tax Treatment which should be discussed with your insurance professional. Qualified plan distributions from a 401(k) and an IRA are subject to income tax while the death benefit is income tax free. If an estate is large enough to trigger estate taxes, the policy can structured in trust to avoid estate and gift taxes.

Loans are not income, according to the IRS. Therefore, any withdrawals taken as loans are not taxable. For retirement purposes, this is advantageous as the distributions from your IUL are not reported on your income tax returns because they are not treated as income. As a result, this money does not affect your social security taxes or Medicare.

The IUL Loan Structure

Tax-free loans are one of the most compelling reasons to consider IUL, especially for retirement income planning. Indexed Universal Life has different loan types, including an indexed or participating loan. The discussion of policy taxation and loans are important ones and a web page is not a sufficient resource to explain these loans. A web page is good for reference but to cover this topic in the best interest of policyholders, it should be done person to person.

Considerations:

- Tax-free distributions and death benefits

- Guaranteed principal protection during negative market returns

- Maximum flexibility

- Favorable policy for premium financing

- Unstructured loans

- Stacked gains from indexed growth

- Less risk

- Caps and participation rates are not guaranteed

- Decreasing surrender charges

- Creditor Protection (varies by state law)

- Living benefits

- Financially strong underwriters

Please contact me at 561-771-4647 or email me to arrange a complimentary consultation about anything on your mind concerning life insurance, annuities or retirement planning.